Some former homeowners unaware that debt may linger

by Catherine Reagor - Nov. 26, 2010 12:00 AM

The Arizona Republic

Short sales allow people to sell their homes for less then they owe on their mortgage to avoid foreclosure. In Arizona, though, some former homeowners are finding they are still in debt to their lenders, even after completing a short sale.

Short sales, unlike foreclosures, are not typically covered by Arizona's anti-deficiency law.

That law protects most distressed homeowners if lenders foreclose. It bars lenders from seeking payment from the borrower if the home doesn't sell for as much as the amount owed on the mortgage.

Some lenders apply the same protection to borrowers who complete a short sale.

But a growing number of former homeowners in metro Phoenix are receiving unwelcome calls and letters from lenders or collection agencies telling them they still owe on mortgages for houses they no longer own.

Because the short-sale concept is designed specifically to help homeowners avoid having to pay their lenders more money, some sellers have been careful to negotiate their deals so the lender, by contract, can't later seek payment. Those who haven't done so are at risk.

"I know that there is a great deal of confusion and uncertainty about this issue," said Michelle Lind, general counsel for the Arizona Association of Realtors. She said that real-estate lawyers differ on which situations are subject to the anti-deficiency statutes but that, depending on the kind of loan and the terms of the short-sale contract, the seller can be liable.

"The law is unclear," she said, "and there are many variables that factor in."

Sellers should tread carefully

Tricia Goldblatt sold her Phoenix home through a short sale last year after losing her job as an executive assistant at an engineering firm. A few months ago, she started receiving calls from a collection agency.

"They are telling me I owe $10,000. I did a short sale to get out from under my mortgage," she said. "I don't have that money. I had to move in with my mom."

Goldblatt said she thought the documents for her short sale specifically stated her liability for both her first and second mortgage would be terminated. But the collection agency said it bought the note on her home-equity loan from her lender and wants to be paid.

Home-equity loans, or second mortgages, appear to be the biggest pitfall in such cases.

Plunging home values in metro Phoenix left many homeowners unable to sell their homes for enough money to cover what they owed on their first mortgages, let alone a second mortgage. In short sales, lenders agree to let homeowners sell for less than what they owe. The seller typically gets nothing, but the lenders are at least paid a portion of the original principal.

Some homeowners can work out deals to close their second mortgages. Often, lenders who issued a home-equity loan will accept $2,000 to $5,000 to let the homeowner walk away from the debt.

Some lenders also seek to recoup more of the debt, requiring sellers to sign promissory notes to pay a portion later.

But many sellers think that once the short sale is completed, they are free of liability. That's when the unwelcome calls can begin.

There usually is a lag between a short sale and when a lender will try to collect on unpaid debt or sell it to a collection agency. It was almost a year after Goldblatt's short sale when she was contacted by the collection agency.

Many real-estate agents working with homeowners on short sales refer them to attorneys or make sure the deal calls for the dismissal of all the debt related to the house. The sales require more paperwork and negotiations and are still relatively new to many agents. And, with short sales at record levels in metro Phoenix and nationally, lenders are continuously updating their guidelines.

"It's tough to figure out who owes what to whom in a short sale," said Margie O'Campo De Castillo, a Phoenix real-estate agent. She said she advises sellers to visit an attorney before closing their deals.

'Deficiency issue is muddy'

Real-estate agents and attorneys say some lenders are forgiving all portions of mortgages not covered by the home's resale. But homeowners shouldn't count on it.

"The short-sale contract controls the liability between the seller/borrower and the lender. The anti-deficiency statutes apply only to trustee sales and judicial foreclosures," said Diane Drain, a Phoenix real-estate attorney. "If the short-sale contract does not provide for a full release of personal liability, then the seller has a high probability of receiving a demand for the deficiency."

Kevin Kauffman of Keller Williams Arizona Realty said some of the big lenders, including Bank of America, have said they are applying Arizona's anti-deficiency law to short sales.

"But it's still important to get it in a signed contract. The deficiency issue is muddy, to say the least," said Kauffman, who has closed 120 short sales this year. "You can talk to 10 different lawyers or real-estate agents and get 10 different answers."

Andrew Houglom hired Kauffman to handle the short sale of his Queen Creek home last year.

"We made sure it said in my documents that the deficiency on my loan was paid in full with the short sale," Houglom said. "I did a lot of research before I did the deal and knew lenders were holding some homeowners liable for part of their loan after a short sale."

Lawsuits are stemming from deficiency judgments. Lenders sue homeowners who don't pay, and then homeowners sue their real-estate agents, accountants or other consultants for not protecting them for the liability.

"My warning is that short sales are very dangerous for the seller," Drain said. "They must get legal and tax advice from someone who does not profit from the short sale."

Monday, November 29, 2010

Sunday, October 31, 2010

Kitchen Upgrades

Did you know that the most popular kitchen countertop is granite? It makes up 40% of all purchases beating out laminate and engineered stone.

Sunday, August 8, 2010

Your Neighborhood...

The Arizona Republic has a cool new tool to give you information on your neighborhood!

Check it out here

Check it out here

Sunday, May 23, 2010

Strategic Defaults

Housing recovery threatened by 'strategic defaults'

Bankers: Credit will tighten as people bail on mortgages

by Catherine Reagor - May. 23, 2010 12:00 AM The Arizona Republic

Homeowners walking away from mortgages because they owe more than their homes are worth will make it more difficult for all borrowers to obtain loans. And a tougher lending climate could stifle sales and delay recovery of the battered Phoenix-area housing market.

That's just one take on the worst Phoenix housing market in history from a group of Arizona banking leaders approached by The Republic for a discussion on the market.

Five current and former banking executives were asked a series of questions on the causes behind the housing crash, prospects for a recovery, the notion of walking away from underwater mortgages and buying a house as a longtime home vs. a short-term investment.

Lenders have taken the brunt of the blame for most of the housing crisis and have been criticized on their efforts to work with homeowners facing foreclosure. Through a series of phone interviews and e-mail exchanges, this was their chance to respond and share their point of view on the housing market.

There is also concern that many homebuyers still see homes as speculative investments and not long-term places to live and invest in. The speculative mentality among Phoenix-area homebuyers led to the 2004-06 boom and contributed to the painful bust. Now, about 40 percent of all Phoenix-area homeowners are underwater. During the past year, more than 60,000 homes in the region have been foreclosed on.

Walking away

People abandoning houses and mortgages they can afford - or walking away, as it is now commonly known as - has become a polarizing issue between homeowners and lenders.

Thousands of Phoenix-area homeowners owe more than their houses are worth and don't want to wait as long as five to 10 years for home values to rebound. Others have unsuccessfully tried to work out loan modifications with their lender. Some believe it's a smart business decision to stop paying on an asset they can't sell for its current value. So a growing number of homeowners are considering walking away or have already done so, committing what has become known as a "strategic default."

Lenders see walking away as a broken contract. They are also concerned if enough homeowners walk away from mortgages, future mortgages will be harder to obtain for everyone as the market adjusts for added risk.

"When individuals walk away from a mortgage, there is a ripple effect that goes far beyond the immediate problem," said Bill Randall, a Phoenix resident and former president of First Interstate Bancorp. "It is likely banks and mortgage lenders will tighten credit standards."

Timothy Disbrow, manager of Wells Fargo Home Mortgage Arizona, said it's never a good idea for borrowers to miss one payment, let alone walk away if they have the ability to pay.

"Strategic defaulters hurt us all. We simply have to be able to trust that when a borrower signs their name, they will honor their commitment," said Candace Wiest, president of Avondale-based West Valley National Bank. "Massive strategic defaults will result in less credit availability. Everyone loses in that scenario."

Amy Swaney, a past president of the Arizona Mortgage Lenders Association, said "a significant number of homeowners walking away will slow the recovery."

Speculating on homes

Part of what drove the housing market down, the lenders said, was an inordinate amount of speculation on houses and irrational expectations about home values.

The speculative mindset among metro Phoenix homeowners must change, they say, to ensure a long-term recovery of the housing market.

There's been a dominant shift from long-term to short-term motivations among metro Phoenix homebuyers during the past decade. Because of the region's reliable increases in home value, people began to count on houses for quick profits.

Swaney said all Phoenix homebuyers were speculators during the boom, even if they didn't realize it.

"As home prices continued to go up, and more people had access to equity in their homes, the pool of buyers continued to grow," she said. "The loans were easy. People didn't think they were doing anything wrong as long as the market kept going up. In 2007, the declining housing market uncovered a massive web of inexperienced speculation."

Swaney said the market can't repeat that cycle or the economy won't fully recover.

Wiest said the housing-speculation problem extended into all levels of the Phoenix housing market.

"A local hairdresser in her 30s told me she owned four homes," Wiest said. "I went home and told my husband either she was an exceptional hairdresser or I was an underachiever bank president because I had no idea how she could afford four homes."

Lenders say the majority of homebuyers cannot continue to think of homes as speculative investments that yield quick returns. The quick-flip mentality that led to Phoenix's boom and bust will push back any permanent rebound in home values.

"Trading houses or viewing them as a short-term investment involves risks that may far exceed the individual ability to deal with them," Randall said. "The financial obligation (of buying a home) is usually very large in relation to the individual's net worth. The (housing and mortgage) markets are volatile. It is not appropriate to think of a home in the same way you would trade stocks."

Wednesday, April 28, 2010

How Foreclosure Impacts Your Credit Score

NEW YORK (CNNMoney.com)

NEW YORK (CNNMoney.com)If you're delinquent on your mortgage, your credit score will suffer. Everyone knows that. The question is, by how much?

Until recently, those answers were hard to come by. Credit bureaus were uncommunicative about expressing, in points, just how much impact different foreclosure types of mortgage delinquencies have on scores.

Recently, Fair Isaac, which developed FICO scores, pulled back the curtain a bit, revealing some estimates of point-score declines following mortgage delinquency problems.

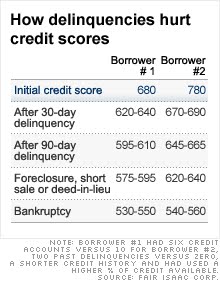

Here are the average hit your credit will take:

30 days late: 40 - 110 points

90 days late: 70 - 135 points

Foreclosure, short sale or deed-in-lieu: 85 - 160

Bankruptcy: 130 - 240

To come to these figures, Fair Isaac created two hypothetical consumers, one who starts out with a fair-to-middling score of 680 and the other with a very good one of 780. (FICO scores range from 300 to 850.)

The hypothetical person with the 780 FICO has 10 credit accounts versus six for the 580, plus a longer credit history, lower utilization of total credit limit and no missed payments on any account. The other consumer has two slightly damaged accounts. Neither have any accounts in collection or adverse public records.

(See the chart above to see how each scenario affected each borrower)

Notice that for both borrowers a single one-time black mark results in steep drops, but it is when they fall further behind that things get really harsh, according to Craig Watts, a spokesman for Fair Isaac.

"The lending industry tends to regard an account differently when it has become 90 or more days late," he said, "The likelihood that consumers will resume paying their overdue obligations drops off significantly after the delinquencies have reached 90 days."

One reason credit companies were so closed-mouthed is that they often can't definitively state how much each delinquencies will affect scores because there are too many variables.

Some borrowers will fall much more steeply than others for the same payment problem, according to Maxine Sweet, vice president for public education at Experian, one of the nation's main credit bureaus.

"If you picture someone who has just one mortgage and one other credit account versus a mature credit user like me with 15 accounts, if they miss one payment that would impact their scores a lot more," she said. "For me, one missed payment would just be a blip."

The point loss also depends on the borrower's starting point: People with very high credit scores have more to lose than low-score borrowers; the impact of a single blemish on an 800 score is more than on a 500.

Of course, it just gets worse when you face foreclosure.

Mortgage borrowers can lose their homes three basic ways: a foreclosure; a short sale, where the home is sold for less than than is owed and the bank (generally) forgives the difference; or a deed-in-lieu, in which the borrower gives back the property and the bank again forgives any unpaid balance.

Sweet said credit bureaus generally slash scores equally for those three resolutions to someone losing their home. The important factor, she said, is that "it's reported that you paid less on a settled account."

Some borrowers may think that because they never missed a payment, they can "walk away" from their homes with relatively little impact on scores. Not true. "When a deed-in-lieu or short sale is reported as a partial payment, it's treated as a serious delinquency," Watts said, "just like a foreclosure."

Even if borrowers made payments faithfully for years before short selling or doing a deed-in-lieu, their credit score will still take a hit. The total decline will run about 85 points for the 680 score borrower to as much as 160 for the 780 score.

Mortgage debt, combined with other financial problems, can send borrowers into bankruptcy, the worst thing that can happen to your credit score.

The effects are long-lasting, according to Sweet. In a Chapter 13 bankruptcy, which involves partial repayment over several years, the stain will take seven years to remove. A Chapter 7 bankruptcy, which involves liquidation, takes 10 years to get over.

Until recently, those answers were hard to come by. Credit bureaus were uncommunicative about expressing, in points, just how much impact different foreclosure types of mortgage delinquencies have on scores.

Recently, Fair Isaac, which developed FICO scores, pulled back the curtain a bit, revealing some estimates of point-score declines following mortgage delinquency problems.

Here are the average hit your credit will take:

30 days late: 40 - 110 points

90 days late: 70 - 135 points

Foreclosure, short sale or deed-in-lieu: 85 - 160

Bankruptcy: 130 - 240

To come to these figures, Fair Isaac created two hypothetical consumers, one who starts out with a fair-to-middling score of 680 and the other with a very good one of 780. (FICO scores range from 300 to 850.)

The hypothetical person with the 780 FICO has 10 credit accounts versus six for the 580, plus a longer credit history, lower utilization of total credit limit and no missed payments on any account. The other consumer has two slightly damaged accounts. Neither have any accounts in collection or adverse public records.

(See the chart above to see how each scenario affected each borrower)

Notice that for both borrowers a single one-time black mark results in steep drops, but it is when they fall further behind that things get really harsh, according to Craig Watts, a spokesman for Fair Isaac.

"The lending industry tends to regard an account differently when it has become 90 or more days late," he said, "The likelihood that consumers will resume paying their overdue obligations drops off significantly after the delinquencies have reached 90 days."

One reason credit companies were so closed-mouthed is that they often can't definitively state how much each delinquencies will affect scores because there are too many variables.

Some borrowers will fall much more steeply than others for the same payment problem, according to Maxine Sweet, vice president for public education at Experian, one of the nation's main credit bureaus.

"If you picture someone who has just one mortgage and one other credit account versus a mature credit user like me with 15 accounts, if they miss one payment that would impact their scores a lot more," she said. "For me, one missed payment would just be a blip."

The point loss also depends on the borrower's starting point: People with very high credit scores have more to lose than low-score borrowers; the impact of a single blemish on an 800 score is more than on a 500.

Of course, it just gets worse when you face foreclosure.

Mortgage borrowers can lose their homes three basic ways: a foreclosure; a short sale, where the home is sold for less than than is owed and the bank (generally) forgives the difference; or a deed-in-lieu, in which the borrower gives back the property and the bank again forgives any unpaid balance.

Sweet said credit bureaus generally slash scores equally for those three resolutions to someone losing their home. The important factor, she said, is that "it's reported that you paid less on a settled account."

Some borrowers may think that because they never missed a payment, they can "walk away" from their homes with relatively little impact on scores. Not true. "When a deed-in-lieu or short sale is reported as a partial payment, it's treated as a serious delinquency," Watts said, "just like a foreclosure."

Even if borrowers made payments faithfully for years before short selling or doing a deed-in-lieu, their credit score will still take a hit. The total decline will run about 85 points for the 680 score borrower to as much as 160 for the 780 score.

Mortgage debt, combined with other financial problems, can send borrowers into bankruptcy, the worst thing that can happen to your credit score.

The effects are long-lasting, according to Sweet. In a Chapter 13 bankruptcy, which involves partial repayment over several years, the stain will take seven years to remove. A Chapter 7 bankruptcy, which involves liquidation, takes 10 years to get over.

It's gonna cost you

Absorbing a big credit-score hit can make many transactions more costly. It's not just paying more for credit card debt and auto loans, insurance can cost more as well.

The average savings for someone with a good versus mediocre credit score is about $115 a year for auto insurance and $60 for home, according to Loretta Sorters, of the Insurance Information Institute.

A low credit score can even make it harder to rent a home because landlords often use credit scores to weed out prospective renters.

Despite the problems a poor credit score can cause, Experian's Sweet recommends that people who are in financial dead ends, like totally unaffordable mortgages, it's better to recognize that and cut your losses quickly; don't prolong the problem.

"You need to do what you need to do to get your finances back in order," she said. "Don't worry about your credit score."

Wednesday, April 21, 2010

New Ways to Tame Credit Card Debt

Mind Over Money by Beth Kobliner (March 2010, Redbook Magazine)

Here are some things credit card companies can and can't do with the new rules and regulations:

1. They can't raise interest rates on debt you've already racked up. One exception: They can hike rates on these existing debts if your payment is more than 60 days late.

2. If your card charges you different interest rates, they must apply your payments to the debt carrying the highest rates first.

3. They can't raise your rates if they find out you've been late on other credit cards or loans.

4. You can no longer go over your credit limit- and be charged the subsequent fees- unless you notify your credit card company in writing that you'd like to spend more than your limit. But you may not want to opt for the right to go over your limit as it will cost you!

5. They will tell you- on your bill- how long it will take to pay off your debt and how much it will cost you, including interest, if you pay only the minimum each month. Get ready for a reality check!

6. Those under 21 years old won't be able to get a credit card unless they show proof of income of get an adult to cosign.

Here are some things credit card companies can and can't do with the new rules and regulations:

1. They can't raise interest rates on debt you've already racked up. One exception: They can hike rates on these existing debts if your payment is more than 60 days late.

2. If your card charges you different interest rates, they must apply your payments to the debt carrying the highest rates first.

3. They can't raise your rates if they find out you've been late on other credit cards or loans.

4. You can no longer go over your credit limit- and be charged the subsequent fees- unless you notify your credit card company in writing that you'd like to spend more than your limit. But you may not want to opt for the right to go over your limit as it will cost you!

5. They will tell you- on your bill- how long it will take to pay off your debt and how much it will cost you, including interest, if you pay only the minimum each month. Get ready for a reality check!

6. Those under 21 years old won't be able to get a credit card unless they show proof of income of get an adult to cosign.

Friday, March 19, 2010

10 Staging Tips to Help Your Home Sell

RISMEDIA, March 19, 2010—(MCT)—

Want to sell your home? Get out the bucket, mop and Mr. Clean. The key to making a positive first impression is simple, said Sandra Rinomato, host of HGTV’s popular “Property Virgins” show.

“Get it clean, clean, clean,” said Rinomato. “If your house isn’t clean, it instantly sends up negative thoughts that the home is not well maintained. If your house is spotless, you’re ahead of the game,” she said.

But don’t stop there, advised Rinomato. To increase your chances of making a sale, “stage” the house to make it as attractive as possible. Until recently, “Staging meant pulling out all the stops—setting the dining table with your best china and crystal, arranging flowers, lighting candles,” she said. “Now we take the minimalist approach. Basically, you want to strip the house to its bare essentials, depersonalize it so potential buyers can superimpose themselves and their lifestyle on the house.”

Rinomato offered the following tips for staging a home:

1. Visit model homes and examine shelter magazines for inexpensive decorating ideas. Always keep in mind you are not decorating for yourself but for the general public.

2. Start with the outside. Give the house a fresh coat of paint, add shiny hardware to the front door and plant a few flowers to send a subliminal message the house is loved and well cared for.

3. Declutter every room to make it look larger. Get rid of family pictures, trophies and knickknacks. Closets and drawers should be no more than 30% full.

4. Invest in eco-friendly but bright lights. Open the drapes or remove them completely. “Light, bright rooms give the impression this is a happy place—and everyone wants to move into a happy place,” said Rinomato.

5. Feature only a few pieces of furniture with mainstream appeal. Pull pieces away from walls to make rooms look bigger.

6. Make sure a room’s primary use is obvious. A bedroom should look like a bedroom, not an office, hobby center or gym.

7. Bedrooms and kitchens are difficult to stage because they are in daily use, but make the effort. Clear everything off the counters and nightstands, roll up the rugs and hide the laundry hamper. Buff the cabinets with car wax and clean under the sinks. Invest in pristine white bed linens and towels.

8. Minimize the “pet effect.” Remove food bowls and litter boxes to the utility room. Deodorize thoroughly.

9. Organize the utility room and garage. Hang up the bicycles, roll up the hose. Renting a storage locker is worth the cost if it helps you sell faster and for a higher price.

10. Once your house is staged, invite your friends or Realtor over and walk them through to get an objective opinion.

Want to sell your home? Get out the bucket, mop and Mr. Clean. The key to making a positive first impression is simple, said Sandra Rinomato, host of HGTV’s popular “Property Virgins” show.

“Get it clean, clean, clean,” said Rinomato. “If your house isn’t clean, it instantly sends up negative thoughts that the home is not well maintained. If your house is spotless, you’re ahead of the game,” she said.

But don’t stop there, advised Rinomato. To increase your chances of making a sale, “stage” the house to make it as attractive as possible. Until recently, “Staging meant pulling out all the stops—setting the dining table with your best china and crystal, arranging flowers, lighting candles,” she said. “Now we take the minimalist approach. Basically, you want to strip the house to its bare essentials, depersonalize it so potential buyers can superimpose themselves and their lifestyle on the house.”

Rinomato offered the following tips for staging a home:

1. Visit model homes and examine shelter magazines for inexpensive decorating ideas. Always keep in mind you are not decorating for yourself but for the general public.

2. Start with the outside. Give the house a fresh coat of paint, add shiny hardware to the front door and plant a few flowers to send a subliminal message the house is loved and well cared for.

3. Declutter every room to make it look larger. Get rid of family pictures, trophies and knickknacks. Closets and drawers should be no more than 30% full.

4. Invest in eco-friendly but bright lights. Open the drapes or remove them completely. “Light, bright rooms give the impression this is a happy place—and everyone wants to move into a happy place,” said Rinomato.

5. Feature only a few pieces of furniture with mainstream appeal. Pull pieces away from walls to make rooms look bigger.

6. Make sure a room’s primary use is obvious. A bedroom should look like a bedroom, not an office, hobby center or gym.

7. Bedrooms and kitchens are difficult to stage because they are in daily use, but make the effort. Clear everything off the counters and nightstands, roll up the rugs and hide the laundry hamper. Buff the cabinets with car wax and clean under the sinks. Invest in pristine white bed linens and towels.

8. Minimize the “pet effect.” Remove food bowls and litter boxes to the utility room. Deodorize thoroughly.

9. Organize the utility room and garage. Hang up the bicycles, roll up the hose. Renting a storage locker is worth the cost if it helps you sell faster and for a higher price.

10. Once your house is staged, invite your friends or Realtor over and walk them through to get an objective opinion.

Tuesday, March 16, 2010

Top 5 Cities Making A Recovery

From Today's Real Estate segment, The Today Show

#3 Phoenix, Arizona (yay!)

Foreclosures: 1 in every 150 homes

Unemployment: 8.2%

Median Home Price: $144,000

Median Home Price Down From 2008: 7.7%

85% of Phoenicians can afford a home

This is great news for the valley!

#3 Phoenix, Arizona (yay!)

Foreclosures: 1 in every 150 homes

Unemployment: 8.2%

Median Home Price: $144,000

Median Home Price Down From 2008: 7.7%

85% of Phoenicians can afford a home

This is great news for the valley!

Friday, February 26, 2010

Back on Market!

Three bedroom, two and a half baths, 1563 square feet in the beautiful master planned community of Village at Spectrum.Only $125,000!

Visit http://www.buyorsellahouseaz.com/ for more details

Friday, January 29, 2010

10 Tips for Settling Into Your New Home

from FrontDoor.com

Shortly after buying a new home, you may feel too overwhelmed with moving boxes and bubble wrap to focus on anything other than getting your stuff from point A to point B. Besides ensuring a smooth moving process, there are several other things you need to take care of as you're getting settled into your home. While you're unpacking, make sure you handle these post-purchase musts:

1. Fill out a change of address form. Visit the local post office or go to the United States Postal Service website to complete an official change of address form. For banks and financial companies, contact them directly to let them know you've moved.

2. Transfer your utilities and services. Change electricity, gas, water, cable, phone and Internet to your new address. Most utilities let you sign up for service or change your existing service online.

3. Secure your home. The previous homeowner's friends and family could have copies of your home's keys, so call a locksmith and have all the outside door locks changed. Also, change the garage door opener codes.

4. Check safety features. Make sure the home's smoke and carbon monoxide detectors have batteries, check the expiration dates on fire extinguishers and make sure all safety devices are in working order.

5. Get to know your home. Find the home's main circuit breaker and make sure it's clearly labeled so you know which breaker turns off which area. Also, find the home's water shutoffs.

6. Map out the area. Take a drive or a walk around the neighborhood to find the nearest grocery store, gas station, bank, hospital and post office.

7. Make it your own. Create a vision for how you'd like to turn your new house into your home. You can start by making simple repairs, painting and adding decorative accessories. Read 5 Fast Ways to Make Your New House a Home for ideas. Also, get a basic set of tools and stock up on cleaning supplies.

8. Review HOA rules. We hope you already did this before you bought your home, but it never hurts to refresh your memory. Homeowners associations often have very strict rules on what changes you can and cannot make to your property, so brush up on them to avoid fines. If your community provides trash or recycling pickup, learn the schedule for these services.

9. Meet the neighbors. Your neighbors can keep an eye on your home when you're away, so introduce yourself to establish a good rapport.

10. Relax. You've survived the home-buying process, so the hardest part is over. Store your closing documents in a safe place. Take a deep breath, and enjoy the feeling of being a new homeowner!

Friday, January 1, 2010

Want to Update Your Home?

10 Big-Impact, Low-Cost Remodeling Projects

1. Tidy up kitchen cabinets

2. Add or replace tile (on the floor or as a backsplash!)

3. Add a breakfast bar

4. Install granite tile instead of a slab

5. Freshen up a bathroom without retiling (a new medicine cabinet? new light fixtures? a new faucet?)

6. Freshen up the basement

7. Add a bedroom (convert a den or a large room into a smaller room and a bedroom)

8. Spruce up cabinet fronts

9. Replace light fixtures

10. Tech up the garage

Want tips tailored to your home? Email me and I'll stop by to talk specifics!

1. Tidy up kitchen cabinets

2. Add or replace tile (on the floor or as a backsplash!)

3. Add a breakfast bar

4. Install granite tile instead of a slab

5. Freshen up a bathroom without retiling (a new medicine cabinet? new light fixtures? a new faucet?)

6. Freshen up the basement

7. Add a bedroom (convert a den or a large room into a smaller room and a bedroom)

8. Spruce up cabinet fronts

9. Replace light fixtures

10. Tech up the garage

Want tips tailored to your home? Email me and I'll stop by to talk specifics!

Subscribe to:

Posts (Atom)